Ownership networks

Ownership networks represent a special type of economic networks, wherein the dynamics of stakeholders or companies are represented by agents in a network. The directed links between agents represent possession or interest.

This field of research poses several challenges, since such ownership links stretch out internationally over the whole world, while available data is mostly limited to country-level. One of our goals is to map these links in a global manner, to accumulate global power based in nation-wide information.

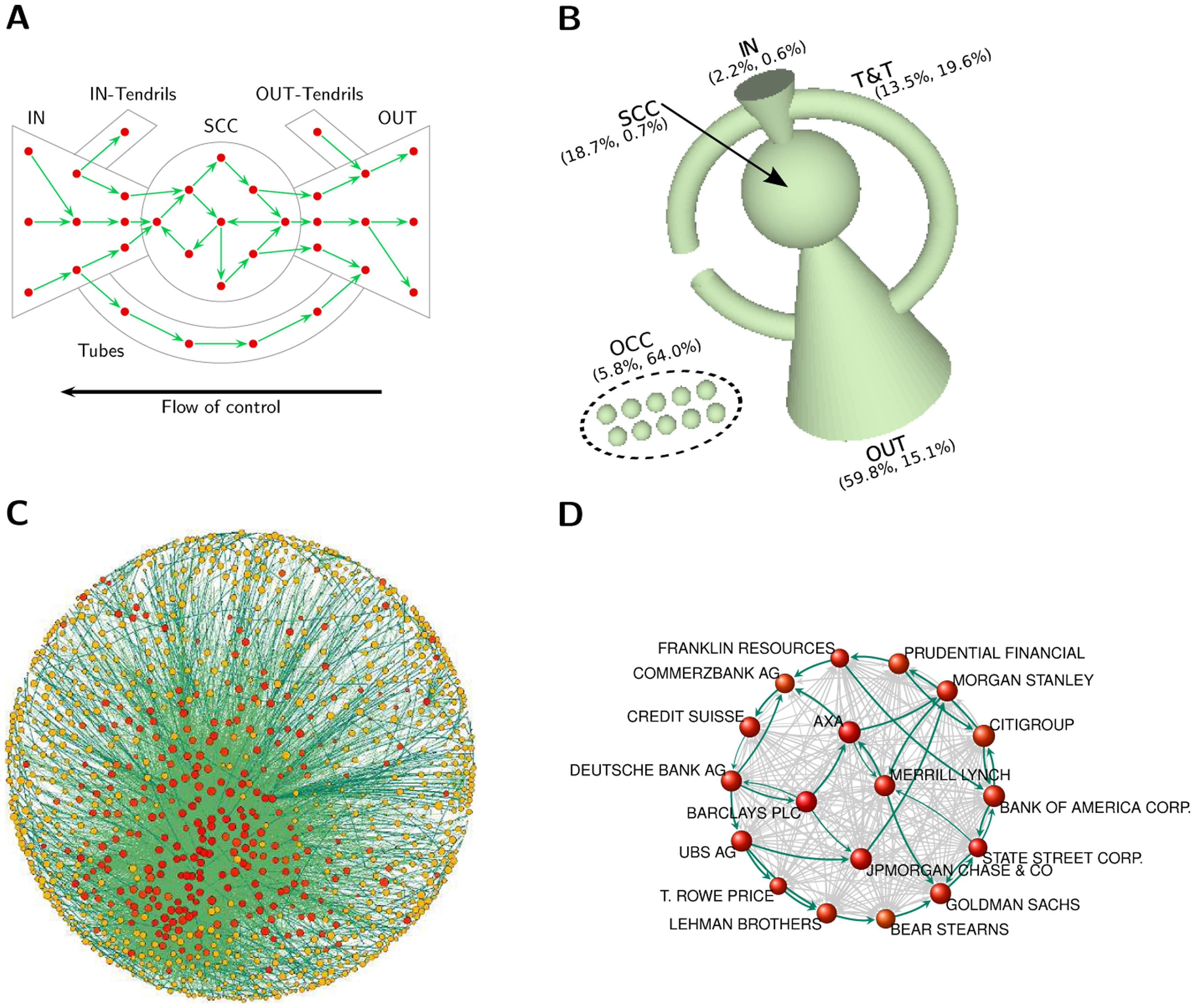

By carrying on the first investigation of the international ownership network architecture, along with the computation of the control held by each global player, we find that transnational corporations form a giant bow-tie structure and that a large portion of control flows to a small tightly-knit core of financial institutions. This core can be seen as an economic "super-entity'', the emergence of which raises important issues both for researchers and policy makers.

The figure shows a representation of a typical bow-tie network architecture (A), and of the structure of a real ownership network (B). The complete empirical ownership network is depicted in (C), while the core nodes are highlighted in (D) together with some cycles.

Geography versus topology in the european ownership network

|

[2011]

|

|

Vitali, Stefania;

Battiston, Stefano

|

New Journal of Physics,

pages: 63021,

volume: 13,

number: 6

|

more» «less

|

Abstract

In this paper, we investigate the network of ownership relationships among European firms and its embedding in the geographical space.We carry out a detailed analysis of geographical distances between pairs of nodes, connected by edges or by shortest paths of varying length. In particular, we study the relation between geographical distance and network distance in comparison with a random spatial network model. While the distribution of geographical distance can be fairly well reproduced, important deviations appear in the network distance and in the size of the largest strongly connected component. Our results show that geographical factors allow us to capture several features of the network, while the deviations quantify the effect of additional economic factors at work in shaping the topology. The analysis is relevant to other types of geographically embedded networks and sheds light on the link formation process in the presence of spatial constraints.

The network of global corporate control

|

[2011]

|

|

Vitali, Stefania;

Glattfelder, James B.;

Battiston, Stefano

|

PLOS ONE,

pages: 1-6,

volume: 6,

number: 10

|

more» «less

|

Abstract

The structure of the control network of transnational corporations affects global market competition and financial stability. So far, only small national samples were studied and there was no appropriate methodology to assess control globally. We present the first investigation of the architecture of the international ownership network, along with the computation of the control held by each global player. We find that transnational corporations form a giant bow-tie structure and that a large portion of control flows to a small tightly-knit core of financial institutions. This core can be seen as an economic "super-entity" that raises new important issues both for researchers and policy makers.

Backbone of complex networks of corporations: The flow of control

|

[2009]

|

|

Glattfelder, James B.;

Battiston, Stefano

|

Physical Review E,

pages: 36104,

volume: 80,

number: 3

|

more» «less

|

Abstract

We present a methodology to extract the backbone of complex networks based on the weight and direction of links, as well as on non-topological properties of nodes. We show how the methodology can be applied in general to networks in which mass or energy is flowing along the links. In particular, the procedure enables us to address important questions in economics, namely, how control and wealth are structured and concentrated across national markets. We report on the first cross-country investigation of ownership networks, focusing on the stock markets of 48 countries around the world. On the one hand, our analysis confirms results expected on the basis of the literature on corporate control, namely, that in Anglo-Saxon countries control tends to be dispersed among numerous shareholders. On the other hand, it also reveals that in the same countries, control is found to be highly concentrated at the global level, namely, lying in the hands of very few important shareholders. Interestingly, the exact opposite is observed for European countries. These results have previously not been reported as they are not observable without the kind of network analysis developed here.

The Network of Inter-regional Direct Investment Stocks across Europe

|

[2007]

|

|

Battiston, Stefano;

Rodrigues, Joao F.;

Zeytinoglu, Hamza

|

ACS - Advances in Complex Systems,

pages: 29-51,

volume: 10,

number: 1

|

more» «less

|

Abstract

We propose a methodological framework to study the dynamics of inter-regional investment flow in Europe from a Complex Networks perspective, an approach with recent proven success in many fields including economics. In this work we study the network of investment stocks in Europe at two different levels: first, we compute the inward-outward investment stocks at the level of firms, based on ownership shares and number of employees; then we estimate the inward-outward investment stock at the level of regions in Europe, by aggregating the ownership network of firms, based on their headquarter location. Despite the intuitive value of this approach for EU policy making in economic development, to our knowledge there are no similar works in the literature yet. In this paper we focus on statistical distributions and scaling laws of activity, investment stock and connectivity degree both at the level of firms and at the level of regions. In particular we find that investment stock of firms is power law distributed with an exponent very close to the one found for firm activity. On the other hand investment stock and activity of regions turn out to be log-normal distributed. At both levels we find scaling laws relating investment to activity and connectivity. In particular, we find that investment stock scales with connectivity in a similar way as has been previously found for stock market data, calling for further investigations on a possible general scaling law holding true in economical networks.

|